Introduction

Momentum trading is an interesting approach to short-term trading. It involves a “strategy to capitalize on the continuance of an existing market trend…(by)…going long stocks, futures, or market ETFs showing upward-trending prices and short the respective assets with downward-trending prices” (Investopedia). Two classic indicators of momentum are the Relative Strength Index (RSI) and the Stochastic Oscillator (STO). In this post, I evaluate the effectiveness of simple RSI and STO trading strategies.

Meet the Indicators

Relative Strength Index (RSI)

The RSI is a momentum oscillator that measures the speed and magnitude of price movements (StockCharts). A nice feature about the RSI is that it is bound between 0 and 100. This enables us to set fixed thresholds to indicate when to buy a stock (because it’s oversold) and when to sell a stock (because it’s overbought). The RSI has three parameters:

- Lookback Period: This the number of days in the past to calculate gains and losses. The traditional setting is 14 periods.

- Oversold Threshold: This indicates the level at which a stock is considered too low, possibly due to overreaction. In theory, oversold stocks are poised for an upward rebound. The traditional setting is 30.

- Overbought Threshold: This indicates the level at which a stock is considered excessively high. The traditional setting is 70.

Stochastic Oscillator (STO)

The STO is also a momentum oscillator, and it measures the relative position of the current closing price within the trading range of the past n days. For example, if the trading range in the past 14 days was $10 to $1000 and the current price is $700, then the STO would give a reading of about 70 (out of 100). The parameters are the same as the RSI, except that the traditional oversold threshold is 20 and the traditional overbought threshold is 80. Refer to StockCharts for a more detailed description of the STO.

Trading Simulation

Next, we run trading simulations to evaluate the effectiveness of the RSI and STO in delivering positive excess returns.

Evaluation Metrics

I use two metrics to evaluate the strategies:

- Annualised Returns: In my first post, I computed the overall returns from MACD-based trading strategies, which resulted in huge variance due to the different time periods used for the various stocks. Thus, in this post, I annualise returns from the RSI/STO trading strategies and the buy-and-hold benchmark.

- Percentage of Profitable Trades: This is simply the Precision metric from my first post, but in simpler terms. It measures the proportion of all trades executed by the RSI/STO strategies that were profitable.

Parameters

I tested the following parameters for both the RSI and STO:

- Lookback Period: 5, 10, 15, and 20

- Oversold Threshold: 10, 20, and 30

- Overbought Threshold: 70, 80, and 90

This amounted to 30 configurations per indicator (RSI/STO).

Data

We used 493 stocks from the S&P 500 to test the trading strategies. In total, approximately 35,500 simulations were run.

# Import required modules

import fix_yahoo_finance as yf

import matplotlib as mpl

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from pandas_datareader import data as pdr

from sklearn.linear_model import LinearRegression

import warnings

from yahoo_finance import Share

# Settings

warnings.filterwarnings('ignore')

# Override pdr

yf.pdr_override()

# Import stocklist

sp500 = pd.read_csv('sp500.csv')

Helper Functions

# Function for simple moving average

def sma(x, n = 200):

# Copy data

df = x.copy()

# Calculate rolling mean

temp_sma = pd.rolling_mean(df.Close, n)

# Output

return temp_sma

# Function for RSI

def rsi(x, n = 14):

# Copy data

df = x.copy()

# Calculate difference

df['delta'] = df.Close.diff()

# Calculate gains and losses

gains = df.delta.copy()

gains[gains < 0] = 0

losses = df.delta.copy()

losses[losses > 0] = 0

# Calculate rolling n-day average of gains and losses

avg_gains = pd.rolling_mean(gains, n)

avg_losses = pd.rolling_mean(losses, n).abs()

# Calculate relative strength

rs = avg_gains / avg_losses

# Calculate RSI

rsi = 100.0 - (100.0 / (1.0 + rs))

# Output

return(rsi)

# Function for Stochastic Oscillator

def stoch(x, n = 14):

# Copy data

df = x.copy()

# Calculate %K

stoch_k = ((df.Close - pd.rolling_min(df.Low, n)) / (pd.rolling_max(df.High, n) - pd.rolling_min(df.Low, n))) * 100

# Output

return stoch_k

# Function for trading simulations

def sim_trade(close, buy_signal, sell_signal, sma_filter, indicator, bah, verbose = False):

# Initialise variables

BUY_STATE = 0

BUY_PRICE = 0

PORTFOLIO_VALUE = 100

TRADES = 0

PROFITABLE_TRADES = 0

RETURNS = []

# Loop through

for i in np.arange(len(close)):

# Check if stock is trading above SMA-200

if sma_filter.iloc[i]:

# Check buy state

if BUY_STATE == 0:

# If buy signal triggered

if buy_signal.iloc[i] == 1:

# Update buy state

BUY_STATE = 1

# Save price

BUY_PRICE = close.iloc[i].copy()

else:

# If sell signal triggered

if sell_signal.iloc[i] == 1:

# Update buy state

BUY_STATE = 0

# Calculate returns

temp_returns = close.iloc[i].copy() / BUY_PRICE

# Update portfolio value

PORTFOLIO_VALUE = PORTFOLIO_VALUE * temp_returns

# Append returns

RETURNS.append(temp_returns - 1)

# Count trades

TRADES += 1

# Count profitable trades

if close.iloc[i].copy() / BUY_PRICE > 1:

PROFITABLE_TRADES += 1

# Compute days

DAYS = len(close)

# Compute annualised returns

ANN_BAH = (1 + bah / 100) ** (250 / DAYS) - 1

ANN_IND = (PORTFOLIO_VALUE / 100) ** (250 / DAYS) - 1

# Print

if verbose:

print(indicator + ' Returns (Total): ' + '{0:.2f}%'.format(PORTFOLIO_VALUE - 100))

print(indicator + ' Excess Returns (Total): ' + '{0:.2f}%'.format(PORTFOLIO_VALUE - 100 - bah))

print(indicator + ' Returns (Annualised): ' + '{0:.2f}%'.format(ANN_IND * 100))

print(indicator + ' Excess Returns (Annualised): ' + '{0:.2f}%'.format(ANN_IND * 100 - ANN_BAH * 100))

print(indicator + ' Mean Returns: ' + '{0:.2f}%'.format(np.mean(RETURNS) * 100))

print(indicator + ' SD Returns: ' + '{0:.2f}%'.format(np.std(RETURNS) * 100))

print(indicator + ' Trades: ' + str(TRADES))

print(indicator + ' % Profitable: ' + '{0:.2f}%'.format(PROFITABLE_TRADES / TRADES * 100))

print()

# Output

return [PORTFOLIO_VALUE - 100, PORTFOLIO_VALUE - 100 - bah, np.mean(RETURNS) * 100, np.std(RETURNS) * 100,

TRADES, PROFITABLE_TRADES, DAYS, ANN_IND * 100, ANN_BAH * 100, bah]

# Function to test configurations

def sim_config(stock, all_n = [5, 10, 15, 20], lower = [10, 20, 30], upper = [70, 80, 90]):

# Initialise list

output = []

# Fix start date and end date

start_date = '1979-01-01'

end_date = '2018-06-01'

# Pull data

orig_df = pdr.get_data_yahoo(stock, start_date, end_date, progress=False)

# Compute SMA-200

orig_df['sma200'] = sma(orig_df)

# FILTER 1: STOCK IS TRADING ABOVE SMA-200

orig_df['f1'] = orig_df.Close > orig_df.sma200

# ---- RSI SIMULATIONS ---- #

# print('Simulating RSI...')

for rn in all_n:

for rl in lower:

for ru in upper:

# Copy data

temp_df = orig_df.copy()

# Compute RSI

temp_df['rsi'] = rsi(temp_df, n = rn)

# Trading signals

temp_df['rsi_buy'] = ((temp_df.rsi.shift(1) < rl) & (temp_df.rsi > rl)).astype(int)

temp_df['rsi_sell'] = ((temp_df.rsi.shift(1) < ru) & (temp_df.rsi > ru)).astype(int)

# Drop missing values

temp_df.dropna(axis = 0, inplace = True)

# Compute buy and hold returns

bah_returns = (temp_df.Close.iloc[-1] / temp_df.Close.iloc[0] - 1) * 100

# Simulate trade

temp_results = sim_trade(temp_df.Close, temp_df.rsi_buy, temp_df.rsi_sell, temp_df.f1, 'RSI', bah_returns)

# Append stock, settings, and simulation results

output.append(

tuple(

[stock, 'rsi', rn, rl, ru] + temp_results

)

)

# ---- STO SIMULATIONS ---- #

# print('Simulating STO...')

for sn in all_n:

for sl in lower:

for su in upper:

# Copy data

temp_df = orig_df.copy()

# Compute RSI

temp_df['sto'] = stoch(temp_df, n = sn)

# Trading signals

temp_df['sto_buy'] = ((temp_df.sto.shift(1) < sl) & (temp_df.sto > sl)).astype(int)

temp_df['sto_sell'] = ((temp_df.sto.shift(1) < su) & (temp_df.sto > su)).astype(int)

# Drop missing values

temp_df.dropna(axis = 0, inplace = True)

# Compute buy and hold returns

bah_returns = (temp_df.Close.iloc[-1] / temp_df.Close.iloc[0] - 1) * 100

# Simulate trade

temp_results = sim_trade(temp_df.Close, temp_df.sto_buy, temp_df.sto_sell, temp_df.f1, 'STO', bah_returns)

# Append stock, settings, and simulation results

output.append(

tuple(

[stock, 'sto', sn, sl, su] + temp_results

)

)

# Output

# print('Done!')

return output

Run Trade Simulations

# Initialise data frame for storage

rsi_stoch_df = pd.DataFrame()

# rsi_stoch_df = pd.read_csv('rsi_stoch_results.csv')

# Collect data on all S&P 500 companies

for i in np.arange(495, len(sp500.Symbol)):

# Get symbol

stk = sp500.Symbol.iloc[i]

# Update

print('Processing [' + str(i) + '] ' + stk + '...', end = '', flush = True)

# Simulate trades and append results

temp_res = sim_config(stk)

# Convert to df

temp_res_df = pd.DataFrame(temp_res, columns = ['stock', 'indicator', 'n', 'lower', 'upper', 'returns', 'exc_returns',

'mean_returns', 'sd_returns', 'trades', 'prof_trades', 'days', 'ann_returns', 'ann_bah',

'bah'])

# Append to data frame

rsi_stoch_df = pd.concat([rsi_stoch_df, temp_res_df], axis = 0)

# Save data

rsi_stoch_df.to_csv('rsi_stoch_results.csv', index = False)

# Calculate excess returns

temp_print_df = temp_res_df[['stock', 'indicator', 'ann_returns', 'ann_bah']].copy()

temp_print_df['ann_exc'] = temp_print_df.ann_returns - temp_print_df.ann_bah

# Print

print('RSI | STO Excess Returns: ' + '{0:.2f}%'.format(temp_print_df.ann_exc[temp_print_df.indicator == 'rsi'].mean()) + \

' | ' + '{0:.2f}%'.format(temp_print_df.ann_exc[temp_print_df.indicator == 'sto'].mean()))

Analysis of Results

In this section, we review the excess returns and percentage of profitable trades from the simulations.

# Load data

rsi_stoch_df = pd.read_csv('rsi_stoch_results.csv')

# Compute annualised excess returns

rsi_stoch_df['ann_exc'] = rsi_stoch_df.ann_returns - rsi_stoch_df.ann_bah

# Compute profitable trades

rsi_stoch_df['profitable_pct'] = rsi_stoch_df.prof_trades / rsi_stoch_df.trades * 100

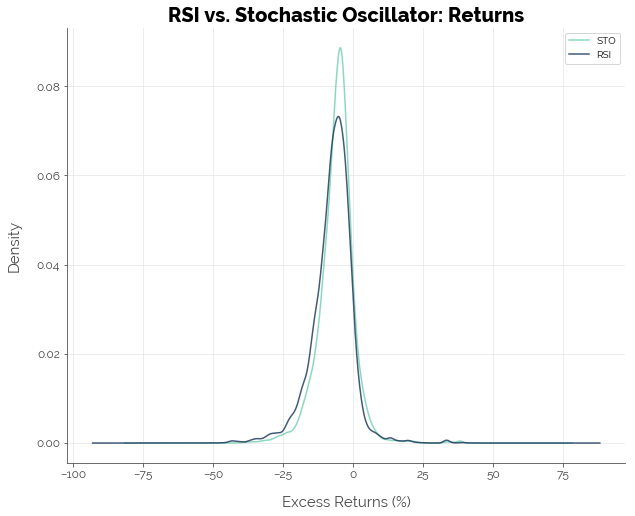

Which Performed Better: The RSI or the STO?

The STO exhibited slightly better performance than the RSI. Approximately 11.4% of all STO strategies delivered positive excess returns, compared to 8.6% for RSI strategies. However, both indicators failed to deliver positive excess returns on average. An interesting thing to note is that although the STO generated more buy signals, the proportion of trades that were actually profitable as predicted by the STO was comparable to that of the RSI.

# Summarise and rank by annualised excess returns

rsi_stoch_df[['indicator', 'ann_exc', 'days', 'trades', 'profitable_pct']].groupby(['indicator']).mean().sort_values(by = 'ann_exc', ascending = False)

| ann_exc | days | trades | profitable_pct | |

|---|---|---|---|---|

| indicator | ||||

| sto | -6.017121 | 6830.234280 | 136.760367 | 75.054938 |

| rsi | -7.609239 | 6826.818458 | 47.954868 | 78.381752 |

Which Setting Performed Best?

Lookback Period (n)

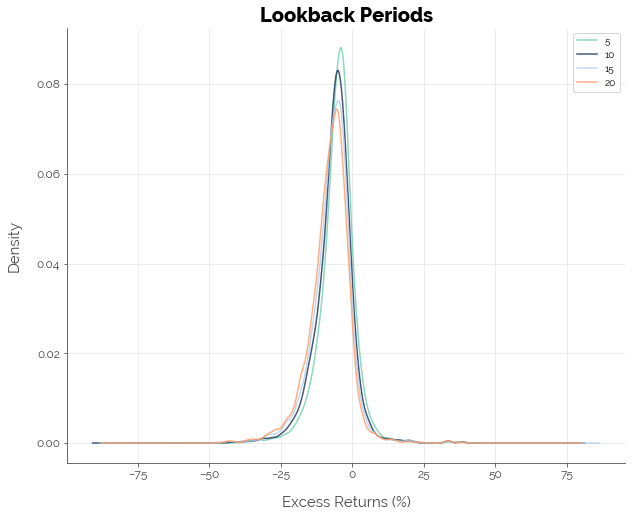

In general, there were minor advantages from using a shorter lookback period. However, once again, all lookback period settings failed to generate positive excess returns on average.

# Summarise and rank by annualised excess returns

round(rsi_stoch_df[['n', 'indicator', 'ann_exc', 'days', 'trades', 'profitable_pct']].groupby(['n']).mean().sort_values(by = 'ann_exc', ascending = False), 2)

| ann_exc | days | trades | profitable_pct | |

|---|---|---|---|---|

| n | ||||

| 5 | -5.31 | 6825.26 | 181.13 | 73.17 |

| 10 | -6.55 | 6829.04 | 88.43 | 76.15 |

| 15 | -7.29 | 6829.75 | 57.40 | 78.45 |

| 20 | -8.11 | 6830.05 | 42.47 | 79.26 |

Thresholds

Like the lookback periods and indicators, average excess returns were negative for all combinations of thresholds (for oversold or overbought signals).

# Create ID for thresholds

rsi_stoch_df['thresh'] = rsi_stoch_df.lower.astype(str) + '-' + rsi_stoch_df.upper.astype(str)

# Summarise and rank by annualised excess returns

round(rsi_stoch_df[['thresh', 'indicator', 'ann_exc', 'days', 'trades', 'profitable_pct']].groupby(['thresh', 'indicator']).mean().sort_values(by = 'ann_exc', ascending = False).head(10), 2)

| ann_exc | days | trades | profitable_pct | ||

|---|---|---|---|---|---|

| thresh | indicator | ||||

| 30-90 | rsi | -3.00 | 6826.82 | 47.03 | 80.96 |

| 20-90 | sto | -4.96 | 6830.23 | 127.87 | 75.29 |

| 30-90 | sto | -5.01 | 6830.23 | 146.06 | 75.77 |

| 30-80 | rsi | -5.21 | 6826.82 | 73.17 | 77.64 |

| 10-90 | sto | -5.44 | 6830.23 | 99.93 | 75.63 |

| 20-90 | rsi | -5.89 | 6826.82 | 37.83 | 80.51 |

| 20-80 | sto | -5.99 | 6830.23 | 142.69 | 75.19 |

| 30-80 | sto | -6.14 | 6830.23 | 165.62 | 75.38 |

| 10-80 | sto | -6.31 | 6830.23 | 108.29 | 75.49 |

| 20-70 | sto | -6.67 | 6830.23 | 151.05 | 74.08 |

Combined Settings

When split by the combined settings (lookback period + oversold and overbought thresholds), there was no difference: no configuration could deliver positive excess returns on average. The increase in the percentage of profitable trades was inversely proportionate to the number of trades. This is what we expect: the fewer signals there are, the more spread out they are likely to be; and the longer you hold a stock, the higher the probability that that trade will be profitable.

# Create ID for combined setting

rsi_stoch_df['full_setting'] = rsi_stoch_df.n.astype(str) + '-' \

+ rsi_stoch_df.lower.astype(str) + '-' + rsi_stoch_df.upper.astype(str)

# Summarise and rank by annualised excess returns

round(rsi_stoch_df[['full_setting', 'indicator', 'ann_exc', 'days', 'trades', 'profitable_pct']].groupby(['full_setting', 'indicator']).mean().sort_values(by = 'ann_exc', ascending = False).head(10), 2)

| ann_exc | days | trades | profitable_pct | ||

|---|---|---|---|---|---|

| full_setting | indicator | ||||

| 15-30-90 | rsi | -1.98 | 6829.06 | 9.70 | 83.13 |

| 10-30-90 | rsi | -2.76 | 6827.73 | 34.70 | 78.13 |

| 5-30-90 | sto | -3.15 | 6829.67 | 233.58 | 73.64 |

| 5-20-90 | sto | -3.23 | 6829.67 | 207.22 | 73.34 |

| 5-30-90 | rsi | -3.34 | 6820.85 | 140.84 | 73.55 |

| 20-30-90 | rsi | -3.92 | 6829.64 | 2.87 | 90.08 |

| 5-10-90 | sto | -3.97 | 6829.67 | 160.34 | 73.38 |

| 5-20-90 | rsi | -4.24 | 6820.85 | 118.02 | 73.93 |

| 5-20-80 | sto | -4.63 | 6829.67 | 237.98 | 73.20 |

| 5-30-80 | sto | -4.73 | 6829.67 | 272.34 | 72.92 |

Which Stocks Performed Best?

The stocks given in the table below were stocks on which the trading strategies beat the market. This does not mean that you can simply apply RSI and STO trading strategies to these stocks and expect a profit in the future, because (1) past relationships between the technical indicators and these stocks’ prices may not persist, and (2) there was something fundamentally wrong with all of these stocks.

First, note how all of these stocks had negative buy-and-hold returns. Second, note how there were so few trades across the simulation window for both the RSI and the STO. When we put these pieces of information together, we realise that, chances are, the RSI and STO trading strategies recommended buying these stocks when they were still climbing, selling these stocks at a profit, and making no further buy or sell recommendations. Consequently, these trading strategies achieved a small profit or loss that were larger (in absolute terms) than the buy-and-hold benchmark returns. That explains why the RSI and STO strategies looked good on these stocks.

Using this new information by considering only stocks that had positive buy-and-hold returns, we can revise our previous statistics on the percentage of RSI and STO trading strategies that delivered positive excess returns from 8.6% and 11.4% to 6.2% and 9.1% respectively.

# Summarise and rank by annualised excess returns

round(rsi_stoch_df[['stock', 'indicator', 'ann_exc', 'ann_returns', 'ann_bah', 'trades', 'days']].groupby(['stock', 'indicator']).mean().sort_values(by = 'ann_exc', ascending = False).head(10), 2)

| ann_exc | ann_returns | ann_bah | trades | days | ||

|---|---|---|---|---|---|---|

| stock | indicator | |||||

| UA | sto | 36.22 | 2.90 | -33.32 | 0.83 | 531.0 |

| rsi | 34.28 | 0.96 | -33.32 | 0.31 | 531.0 | |

| KHC | sto | 17.39 | 3.92 | -13.47 | 8.92 | 534.0 |

| EVHC | rsi | 17.31 | -2.25 | -19.56 | 3.39 | 1009.0 |

| sto | 15.99 | -3.57 | -19.56 | 10.36 | 1009.0 | |

| KHC | rsi | 14.79 | 1.32 | -13.47 | 2.50 | 534.0 |

| NAVI | sto | 11.11 | 0.59 | -10.51 | 10.83 | 839.0 |

| rsi | 10.97 | 0.46 | -10.51 | 4.61 | 839.0 | |

| COTY | rsi | 8.33 | 5.44 | -2.89 | 6.58 | 1052.0 |

| JNPR | rsi | 8.18 | -0.31 | -8.49 | 24.00 | 4565.0 |

Conclusion [TLDR]

In conclusion, we found no evidence that the RSI and STO trading strategies could beat the buy-and-hold benchmark. The STO generated more buy/sell signals and performed slightly better than the RSI. However, both performed poorly on absolute terms: only 6.2% of RSI trading strategies and 9.1% of STO trading strategies for stocks with a positive buy-and-hold return generated positive excess returns. Traders will need to incorporate other technical indicators in their trading strategies to increase their chances of beating the buy-and-hold benchmark.

Click here for the full Jupyter notebook.

Credits for images: FinanceAndMarkets.com